| The Legal Limit Algo – Table of Contents

|

Update 04/06/2012: We have determined the quoting sequences identified in this article are generated by the BATS Market Maker Quoter, the BATS exchange’s Automatic Market Maker.

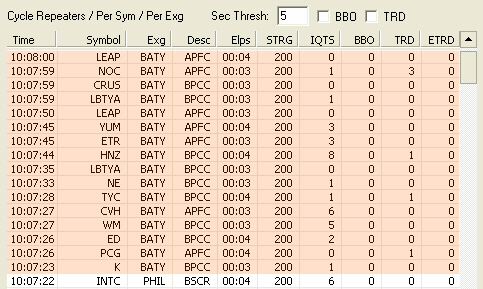

On June 28, 2011 while working on our algo monitoring application, we noticed large numbers of bidprice/askprice climb/fall sequence cycles, all originating from the BATY exchange:

The sequences were very curious and involved very liquid issues. Upon further examination we discovered what we termed “The Legal Limit” algo, as its order prices climb and fall from the tip of the required BBO distance thresholds to the current price range and then repeating.

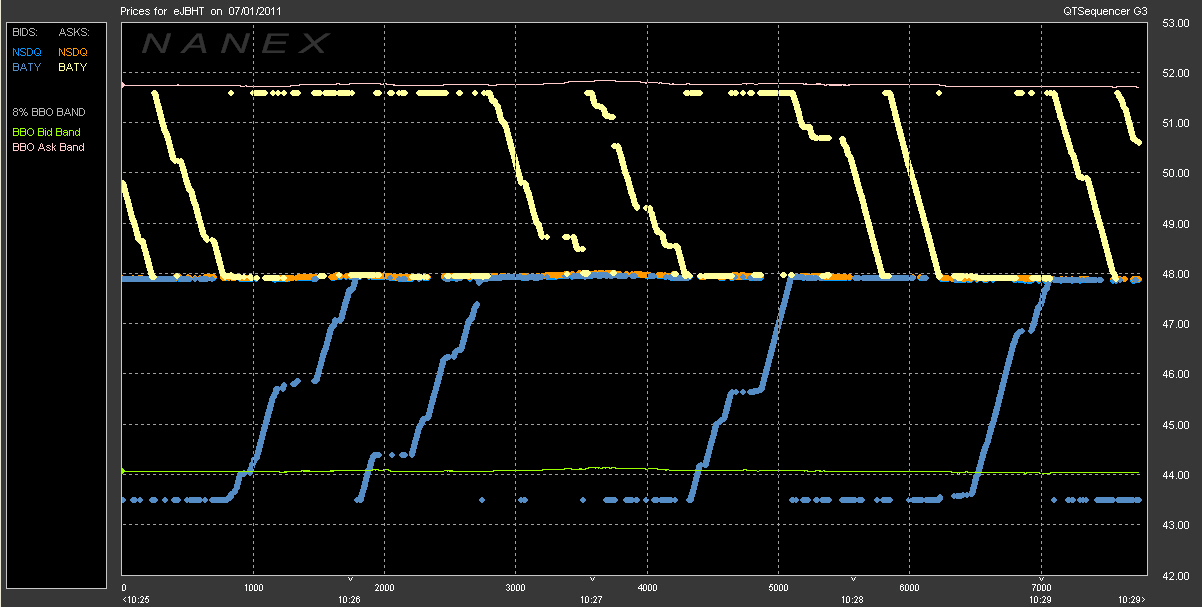

Symbol JBHT – 5 second glimpse of the algo on 07/01/2011 (click on chart for a high resolution image).

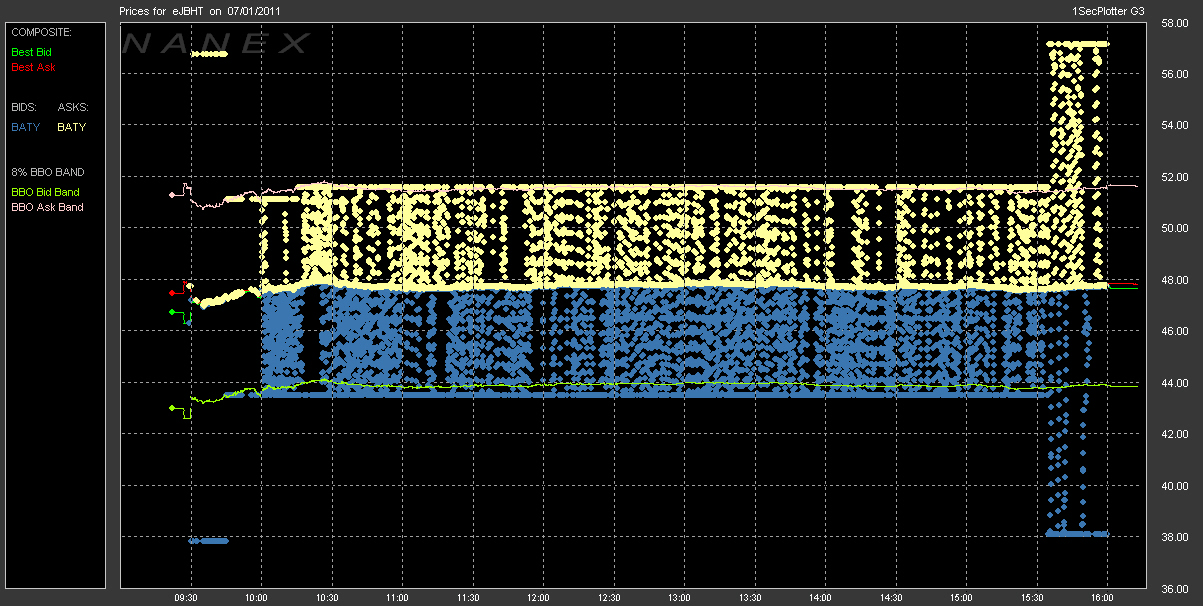

Symbol JBHT – The entire trading day of 07/01/2011 (click on chart for a high resolution image).

What we know about the algo to date:

- The algo runs in highly liquid issues. There appears to be no particular class of stock, we have seen the algo in dozens (a conservative estimate) of individual issues.

- The algo consistently quotes prices that rise and fall from the outer BBO distance thresholds to the current price levels. The distance thresholds are not computed in real-time but are adjusted periodically, or when the timeframe requires a threshold change (see Part 2).

- We have seen excessively high quote rates from this algo. Millions of non-sense quotes over the course of a day.

- The algo runs non-stop, all day long on the selected issues.

- The algo quotes almost exclusively from the BATY exchange. This is not to imply the BATY exchange is responsible for the algo, only that whoever is making these orders is doing so through the BATY exchange. We have seen minor instances of the algo running on the BATS exchange but they are very rare.

- After reviewing data from historical tapes, the first day we see this algo appear is June 20’th, 2011, although running at much lower frequencies than June 28’th, 2010 when first spotted in our algo monitors. As of this writing (July 11’th, 2011) the algo has run every trading day since. It runs on dozens of issues each trading day.

The following pages provide a detailed analysis of the algo and it’s behavior:

- Part 1 – A detailed breakdown of the algo running in one issue.

- Part 2 – The algo is aware of the limits/timeframes in individual issues.

- Part 3 – The algo runs all day.

- Part 4 – Finer details.

- Part 5 – Additional examples

Click here to see the SEC rules prohibiting Market Maker stub quotes which went into effect in December 2010.

Click here to see stocks in the Russell 1000.