|

| III. The NBBO

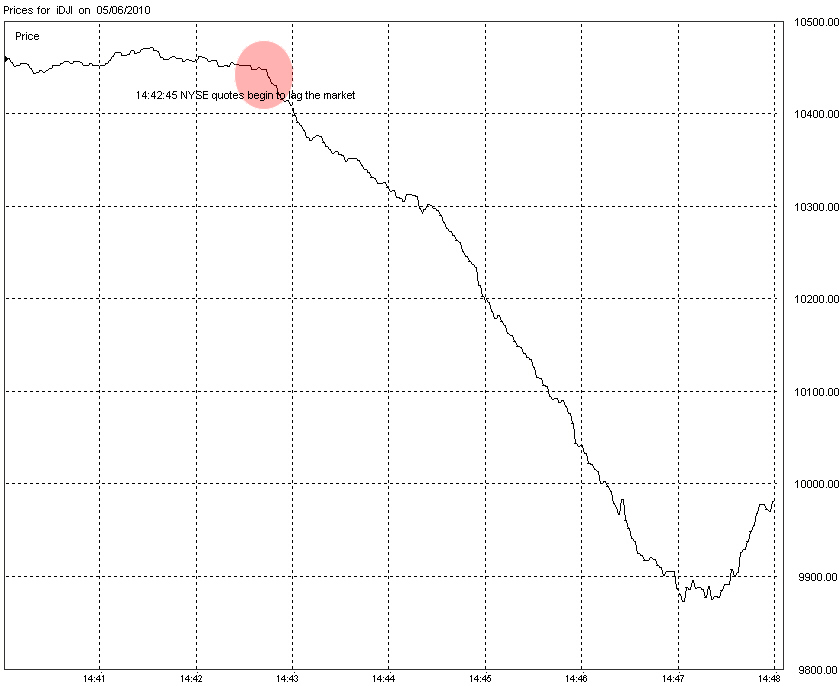

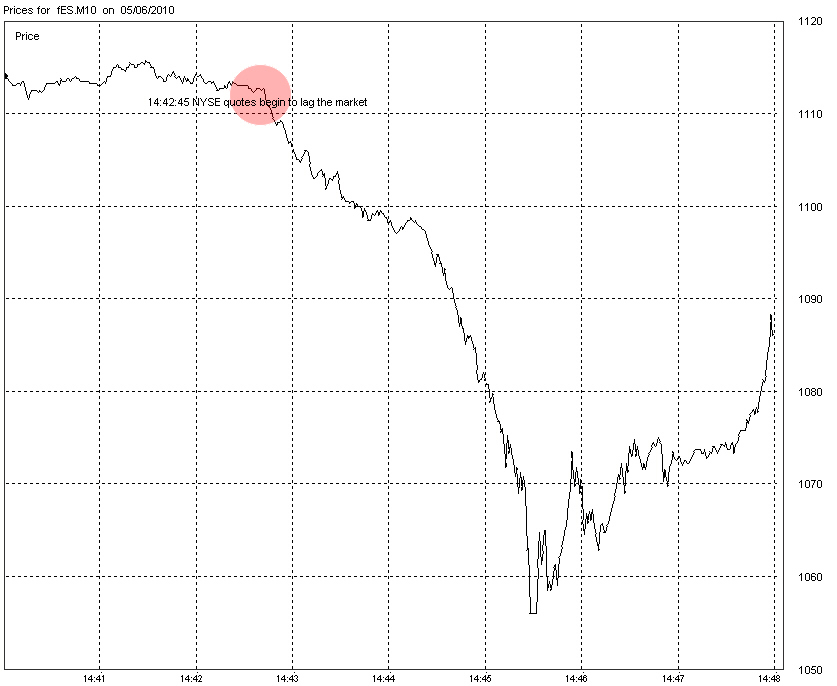

As we have reported, as the NYSE quotes that were lagging were time stamped as current, CQS (responsible for determining the NBBO) would designate NYSE quotes as the NBBO even though the quotes were stale and crossed with other markets. On 05/06/2010 there were approx 3,300 stock listed on the NYSE exchange. As 1665 stock were determined to have delays and were incorrectly designated as the NBBO, approx. 50% off all stocks listed on the NYSE had incorrect NBBO pricing. Therefore any analysis using the NBBO for these stocks after 14:42:45 would be invalid.

IV. Importance of CQS/CTS

Shown above are four paragraphs (from two separate pages) regarding how many firms were effected by CQS/CTS and in fact influenced by CQS/CTS in trade decisions, regardless of receiving premium feeds, CQS/CTS or both. Again from page 78:

Loss of liquidity really means buyers pulled out — few buyers means lower prices. The reason the buyers pulled out? As evident by the SEC’s statements above, one of the primary reasons was lack of confidence in data integrity and much of that was due to delays experienced on the NYSE. In regards to volatility levels when trades began to hit stub quotes, actual execution of trades at stub quotes did not begin to occur until the market had bottomed and played no role in the actual crash itself. Furthermore, from Page 76:

As stated in Item II of this report, approx. 50% of all NYSE stocks had incorrect NBBO values after 2:42:45. A simple search for “NBBO” in the report is all that is needed to determine how much of the analysis relies on the NBBO (and NBBO mid-point). Given this, 50% of the analysis in the report which uses the NBBO for NYSE listed stocks after 14:42:45 must be considered void, as the NBBO was incorrect. This should underscore the importance of CQS/CTS. |

|

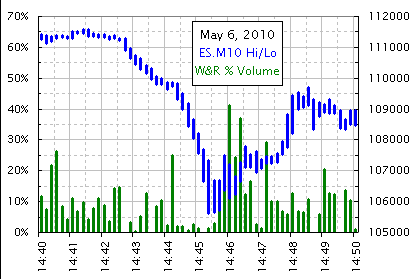

V. Time Stamping of Quote Data As we reported in both our Initial Flash Crash Report and Flash Crash Summary Report, when quotes from the NYSE were lagging the market, they were time stamped when disseminated from CQS and not when the orders were placed. Therefore the orders appeared to be current (which led to the NYSE bids being designated as the NBBO even though they were severely crossed with other markets). This was a key issue — the lag in NYSE quotes was not detected and sell order flow routed to the NYSE. Proper time stamping of quotes should be the cornerstone of market structure and should apply equally to both proprietary exchange feeds and CQS/CTS. When quotes that are 20 seconds (or more) behind the real market and time stamped as current, the ability to detect latency in that feed is diminished significantly. This is most likely the reason no one knew the NYSE feed was delayed (including the NYSE). Changing the current procedure to time stamp at the time a quote or trade is generated is a near trivial exercise. It probably comes as a surprise to many that time stamping isn’t done this way now. In both our initial and summary reports we make this recommendation. Despite the ramifications of incorrect time stamping, the issue is not addressed in the report. VI. Data Used There are currently 11 reporting exchanges for US securities (NYSE, Nasdaq, ISE, BATS, Boston, Cincinnati (National Stock Exchange), CBOE, ARCA, Chicago, EDGX and EDGA). The SEC report analyzed data from 5 exchanges which represented 90% of trade executions on 05/06/2010.

The majority of the analysis appears to have been conducted with 1 minute shapshot data or 15 minute interval data. At best, one minute snap-shot data shows what the data looked like at the end of (or start of — the report does not specify) each minute. 5,000 stocks using one-minute snap-shot data would represent 5,000 data points. However, actual exchange data would represent 12 million data points. So essentially, 1/2400 of the data available was examined. In regards to the analysis of HFT trading using 15 minute data increments, many HFT algorithms quote at rates exceeding 5,000 orders per second. VII. Other Omissions

|